Duration: 30 minutes

Learning Objectives:

•Understand how credit cards work and their impact on financial health

•Use credit cards strategically without falling into debt

•Build credit score through responsible use

•Recognize and avoid credit card traps

Content Outline:

4.1 Credit Card Fundamentals (8 min)

•How credit cards differ from debit card

What a debit card is

-

Spends your money (comes straight from your checking account).

-

If you have $200 in the account, you can spend about $200.

-

Helps avoid debt, but you can still get hit with overdraft fees if you spend more than you have (depending on your bank settings).

What a credit card is

-

Borrows money from the card issuer (a revolving loan).

-

You get a bill later. If you don’t pay the full statement balance, you pay interest (often high).

-

Builds credit history when used responsibly.

Key differences that matter most

-

Fraud protection: Credit cards usually offer stronger consumer protections and easier chargebacks than debit (because it’s the bank’s money on the line first).

-

Cost of mistakes: With debit, a mistake can drain your account immediately. With credit, the danger is carrying a balance and paying interest for months/years.

-

Credit score: Debit cards don’t build credit. Credit cards can (on-time payments + low utilization help).

-

Spending psychology: Debit feels like spending real money now. Credit can feel “lighter,” which can lead to overspending.

The simplest “best practice”

-

Use debit for day-to-day needs if you’re rebuilding habits.

-

Use credit only if you can pay the statement balance in full every month (treat it like debit).

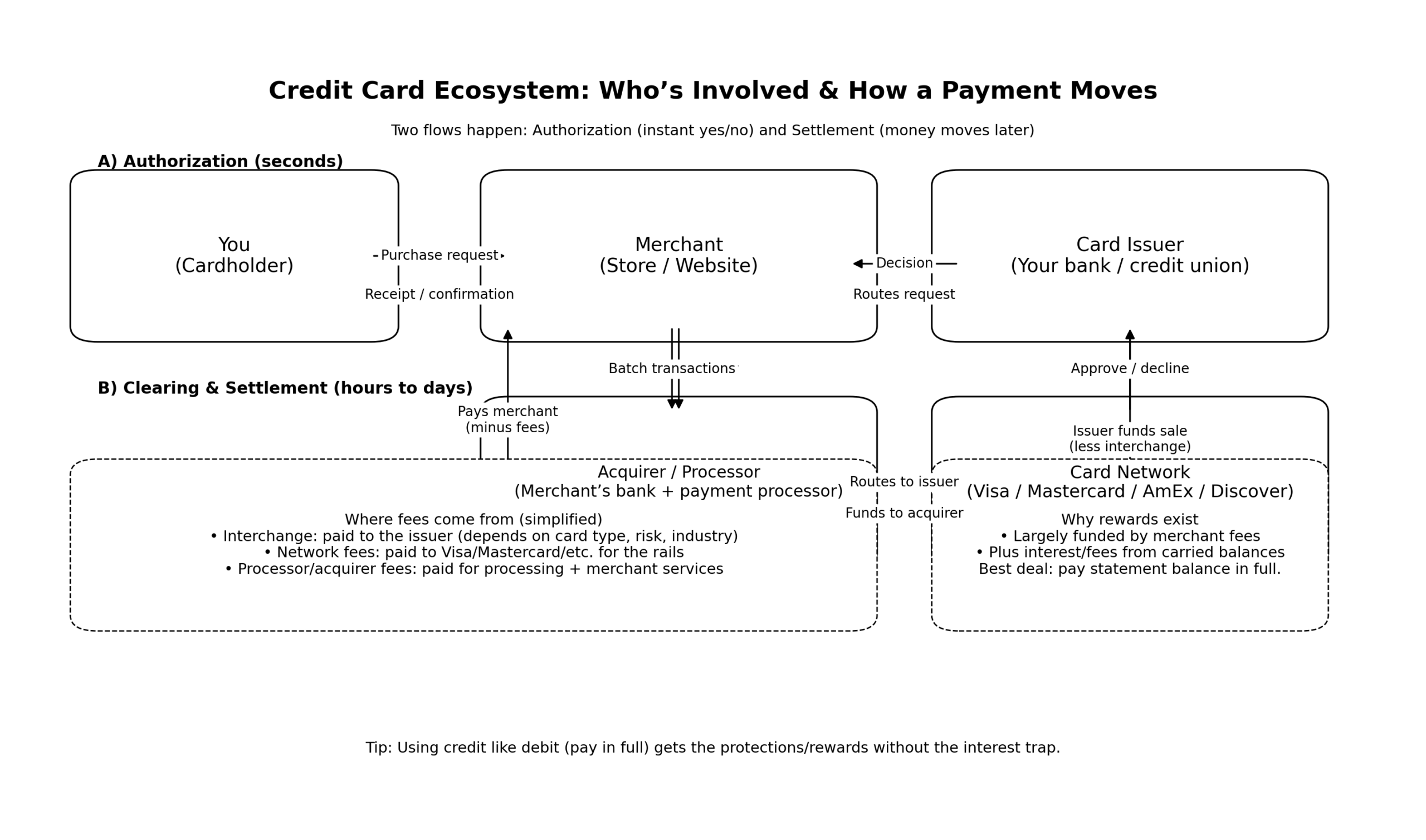

•The credit card ecosystem (you, merchant, card issuer, network

The 4 main players

1) You (the cardholder)

-

Swipe/tap the card to buy something.

-

Agree to repay the issuer (and interest/fees if you don’t pay in full).

2) The merchant (the store/business)

-

Sells you the product/service.

-

Pays fees to accept cards (because they’re getting faster, safer payments).

3) The card issuer (your bank/credit union)

-

Examples: Chase, Capital One, AmEx (also a network), your credit union.

-

Approves/declines your purchase.

-

Sends you the monthly statement.

-

Earns money from interest (if you carry a balance), fees, and a share of transaction revenue.

4) The card network (the rails)

-

Examples: Visa, Mastercard, AmEx, Discover

-

Runs the payment network that routes the transaction between banks.

-

Sets rules/standards for how card payments work.

-

Takes a small cut of each transaction.

What happens when you tap your card

-

Authorization: Merchant asks, “Will you approve $X?”

-

Network routes it: Visa/Mastercard sends the request to your issuer.

-

Issuer decides: Approve/decline based on fraud checks + your available credit.

-

Clearing & settlement: Later (often 1–2 days), money moves:

-

Issuer pays the merchant’s bank (through the network)

-

Merchant receives the sale amount minus fees

-

-

You repay: You pay the issuer by the due date (full balance = usually no interest; otherwise interest accrues).

Where the fees come from (why merchants pay)

When you pay $100:

-

Merchant pays a fee bundle often called “interchange + network + processor” (varies by card type and merchant setup).

-

Merchant gets something like $97–$99+ depending on fees.

(That’s part of why some places have minimums or prefer cash.)

Why rewards exist

Rewards are basically funded by:

-

Merchant fees (a big part)

-

Interest and fees from people who carry balances (often called “revolvers”)

-

Issuer marketing budgets

So the system rewards people who pay in full, and profits most from people who don’t.

•Key terms: APR, grace period, minimum payment, credit limit

•How card companies make money (interest, fees, merchant fees)

•Why minimum payments keep you in debt forever

Example:

$2,000 balance at 22% APR, $40 minimum payment

•Time to pay off: 7 years

•Total interest paid: $1,741

•Total cost: $3,741 for $2,000 spent

4.2 The Credit Score Connection (10 min)

What is a Credit Score?

•FICO score range: 300-850

•What it affects: Loans, apartments, jobs, insurance rates

•Building credit in your 20s sets you up for decades

Score Factors:

1.Payment history (35%) – Pay on time, always

2.Credit utilization (30%) – Keep under 30% of limit, ideally under 10%

3.Length of credit history (15%) – Start early, keep accounts open

4.New credit (10%) – Don’t apply for multiple cards quickly

5.Credit mix (10%) – Variety helps but not essential when young

Building Credit the Smart Way:

•Start with secured card or student card (lower limits)

•Use for small recurring bills (Netflix, phone)

•Set up autopay for full balance

•Check credit score monthly (free through many apps)

•Goal: Excellent credit (740+) by age 30

4.3 Strategic Credit Card Use (7 min)

The Golden Rule: Never charge more than you can pay in full this month

When to Use Credit Cards:

•Large purchases for buyer protection

•Online shopping for fraud protection

•Travel for insurance benefits

•Earning rewards on planned spending

•Building credit history

When NOT to Use Credit Cards:

•Can’t afford to pay in full

•Impulse purchases

•Trying to “stretch” your budget

•Emotional spending

•Cash-only budget categories (helps control spending)

Maximizing Benefits, Minimizing Risk:

•Choose card with no annual fee (when starting)

•Look for rewards that match your spending (cash back easiest)

•Pay balance weekly (can’t overspend if you pay as you go)

•Set spending alerts

•Treat like debit card (only use money you have)

4.4 Avoiding Credit Card Traps (5 min)

Common Traps:

1.Balance transfers – “0% for 12 months!”

•Balance transfer fee (3-5%)

•High rate after promotional period

•Only works if you stop using cards and pay aggressively

2.Cash advances – Immediate interest, high fees, desperate move

3.Credit limit increases – Opportunity to overspend

4.Reward chasing – Spending more to earn rewards defeats the purpose

5.Store cards – High rates, limited use, clutters credit

Action Plan if You’re Already in Credit Card Debt:

•Stop using cards immediately (freeze in ice if needed)

•Pay more than minimum, focus on highest rate first

•Consider balance transfer only if you commit to payoff plan

•Seek help if overwhelmed (nonprofit credit counseling)

Interactive Elements:

•Credit Card Calculator: See impact of different payment amounts

•Credit Score Simulator: How actions affect your score

•Card Comparison Tool: Find best card for your situation

•Quiz: 10 questions on strategic credit card use

Downloadable Resources:

•Credit Card Payoff Plan Template (Excel)

•Credit Score Building Checklist (PDF)

•Credit Card Agreement Decoder (what to look for – PDF)

•Emergency Credit Card Use Protocol (PDF

{kind=link}